IFRS16 overview

As of 1st January the new lease accounting standard IFRS16 applies.

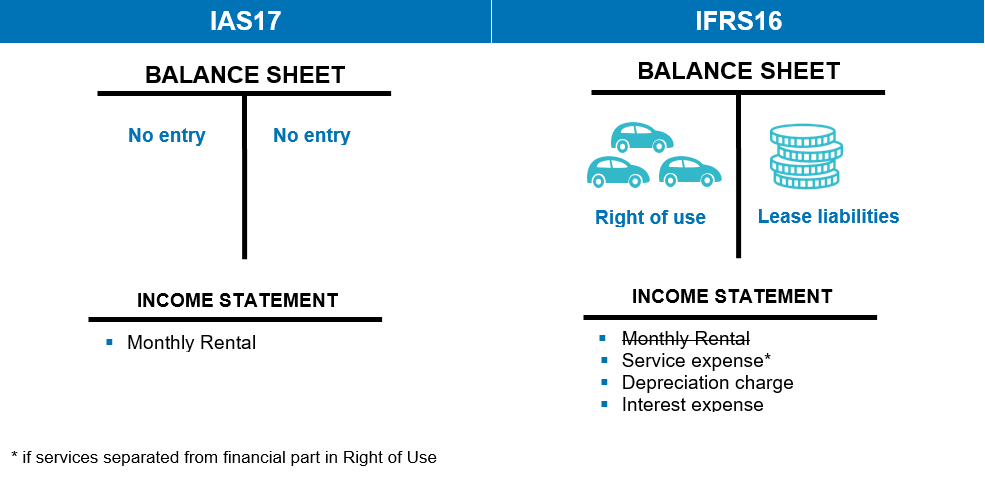

It regulates lease contracts that imply a right of use an asset and replaces IAS17, the standard which applies so far. We have summarized the most important changes in balancing, the advantages and some reporting possibilities for you.

Affected companies

The changes apply for all companies, who set up their balance sheets with IFRS. Not concerned are contracts with a duration below 12 months or with expiration before 01/01/2010 and material assets below USD 5.000.

IAS17 vs. IFRS16

Benefits

- Transfer of risk to lease company

- Greater visibility of the level of debt linked to leasing

- Amounts in the Balance Sheet remain lower than with outright purchase (Right of Use < list price, because residual value is not included)

- Avoidance of using own capital for financing fleet

- EBITDA improvement

ALD Automotive reports

Upon request we can provide different reports to our customers. All monthly lease installments split into finance and service components can be viewed at a glance. We also provide all relevant contract data.

Main IFRS16 Fleet Report

This report contains data covering all requirements and options of IFRS text. We provide also snapshot situations at cut-off dates and a daily feed.

Events Report

If vehicle delivery, contract modification or vehicle return – with the event report you have an overview over your events and also over different periods.

Foot Notes Report

This report allows to take also data for cars ordered but not yet delivered as well as future cash flows into account.

If you have any questions, simply contact us. We are happy to help.